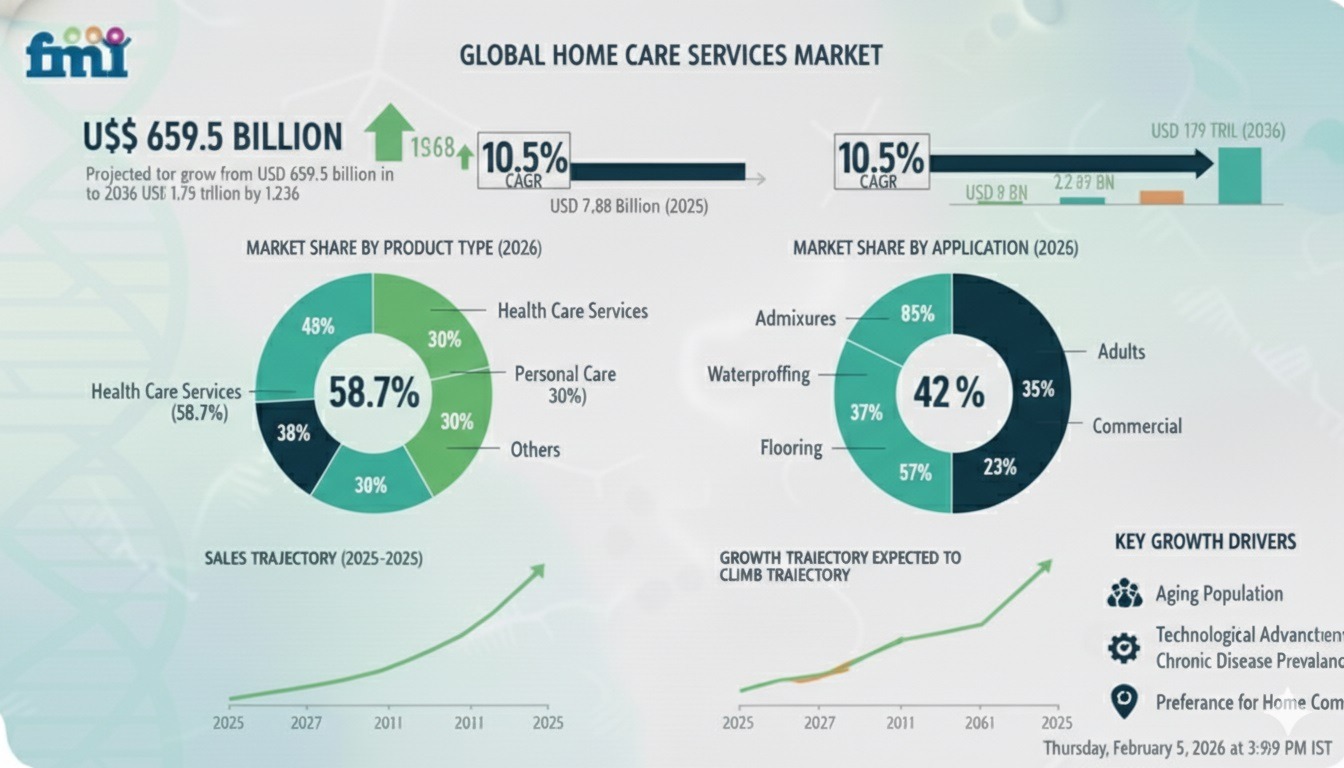

The global home care market is estimated to reach US$658.20 billion in 2026, according to Coherent Market Insights. This growth represents a shift in healthcare models where the geriatric segment accounts for 54.1% of the total market share. For the financial technology sector, this demographic shift has moved beyond health discussions into the realm of wealth management and payment logistics. As families face the rising costs of longevity, fintech tools are becoming the primary mechanism for managing the high price of aging in place.

The financial friction of high-cost care

In New York, the economic pressure of long-term care is visible. On January 1, 2026, the home care minimum wage in New York City, Long Island, and Westchester increased to US$19.65 per hour, as reported by the New York State Department of Labor. While this increase addresses workforce retention, it creates margin pressure for providers and higher out-of-pocket expenses for families.

The 2026 NYC True Cost of Living Report found that 60% of families with adults aged 65 and older in New York City do not have the resources to meet the local cost of living threshold. This gap between income and the price of essential services has necessitated new financial solutions. Families are increasingly turning to digital wallets and specialized savings platforms to manage Medicaid spend-downs and private pay supplements. This financial strain is a major factor in why many seniors are choosing home care over traditional facilities, as they attempt to balance personal preferences with limited budgets.

Fintech and AI operations in home care

The administrative burden of managing long-term care often leads to revenue loss and delayed services. By 2026, AI-driven systems will have begun to automate 40% to 60% of routine claims and referral approvals. According to Clarity Benefit Solutions, these automated processes reduce error rates by approximately 40% while lowering administrative costs per claim.

In a market as complex as New York, fintech innovators are building platforms that integrate with Medicaid-managed care plans and Managed Long Term Care (MLTC) providers. These systems help families track their eligibility and automate payments to ensure care remains uninterrupted. Digital tools now handle the intricacies of New York’s Medicaid waivers, which often require precise documentation and timely financial reporting.

Balancing human service with digital finance

Established organizations like Caring Professionals provide an example of how traditional service models function within this digital-first economy. As a provider of home care services CaringProfessionals manages the coordination of care for over 5,000 patients across New York’s diverse cultural populations. Agencies of this scale must balance personal interaction with the logistical demands of modern payroll and billing systems.

The role of such providers is to maintain the quality of personal interaction while using backend technology to navigate rising labor costs and regulatory changes. In the current economy, the success of a home care agency depends on its ability to process complex insurance claims and manage a large workforce through automated payroll platforms that comply with the US$19.65 hourly minimum.

The rise of specialized insurance-tech

The silver economy has prompted a change in how insurance products are structured. According to a 2026 guide from AITUDE, health insurance models now use machine learning to offer more accurate risk evaluations and faster onboarding. These AI models analyze medical and prescription history to provide personalized premium rates, which can lower the financial barrier for families seeking home-based assistance.

Real-time claims processing has become a standard expectation. When a medical record is submitted, algorithms instantly verify eligibility and compare invoices against policy terms. This reduces the time for claim approvals from several days to a few minutes. However, even with these advances, the industry faces challenges as Medicare policies for health aides continue to shift, affecting how nursing homes and home care agencies receive federal funding.

Future of the longevity economy

The intersection of health and wealth is no longer a niche market. North America currently holds a 35.3% share of the global home care market, driven by a preference for home-based care over institutional settings. As reported by Morningstar, the home care services market is projected to grow to US$1.79 trillion by 2036.

Fintech companies are focusing on this longevity crisis by creating products that address the specific needs of the elderly. This includes predictive analytics to forecast future care costs and automated compliance tools that track changing state regulations. The goal of these innovations is to make the rising cost of care manageable through better data and faster financial transactions. While technology manages the numbers, the focus of the industry remains on sustaining the infrastructure that allows the aging population to remain in their homes.